Even if you have bad credit, you still need to drive. And you still need to live somewhere. Here’s how.

I had a colleague who never paid for anything by credit card. Why?

Because he didn’t believe in credit cards? No.

Because he was allergic to plastic? No.

Because he had bad credit.

There is a stigma attached to bad credit. As this finance blogger puts it:

‘We live in a society that encourages us to overspend and take on credit that we can’t afford, but then shames us heavily when we miss a payment.”

It might be the word “bad”, but bad credit just sounds bad. And people with bad credit just somehow sound bad, too. But they aren’t.

Bad credit happens when things don’t go right. This can happen in several situations:

- Job loss or some other sudden or long-term loss of income

- Unexpected costs, such as medical costs of damage not covered by insurance

- Addictions (gambling, drugs, shopping, etc.), which can place a family in huge debt

If any of these happen when a family is already in debt more than it should be, the results can be catastrophic. For instance, if you are in debt up to your eyeballs and you unexpectedly lose your job, it could put you over the edge.

The result is often bad credit, even bankruptcy.

But it’s not the end of the world.

If you find yourself in that situation, you will also find that life goes on. Except it’s a little different. As my colleague showed me, there is always a way . Sometimes, there is more work involved. Sometimes he had to get certified checks or take out extra cash from the bank.

Yes, you use cash and debit cards. Actually, I use almost only debit cards these days. Cash only when necessary, credit only for automated payments. So that part isn’t that hard.

But I’m not lining up to buy a house or a car. If I was, I am fairly sure that my debit card would go Ka-boom! on me.

So what does one do?

“Just about anyone can get a car loan these days. If you have bad credit don’t be discouraged because in many cases you can get approved if you have been at your job for a while” Take a look at the guideline set forth by https://www.moneyexpert.com/loans/car-finance-loans/car-loans/. Where there’s a will there’s a way and especially with people that want to sell you cars.

Just as with smaller spending, don’t even try the conventional route. The banks won’t touch you. That’s because everything they do is based on formulas that apply to typical folks and “most desirable” customers. There are plenty of people with bad credit, but they are a minority. And they are not the “most desirable” customers.

But there are services that cater to people with bad credit. Where there’s a market, there’s a business catering to it. Is there a catch? Yes. Just as with smaller purchases, you might have a little extra work to do and it might cost you a little more. Good credit reduces your interest rate. Bad credit increases it. That’s a financial law of gravity; you can’t change that.

But you can get a loan, even with bad credit, and you can work to improve your credit in order to get a better rate when renegotiating the loan.

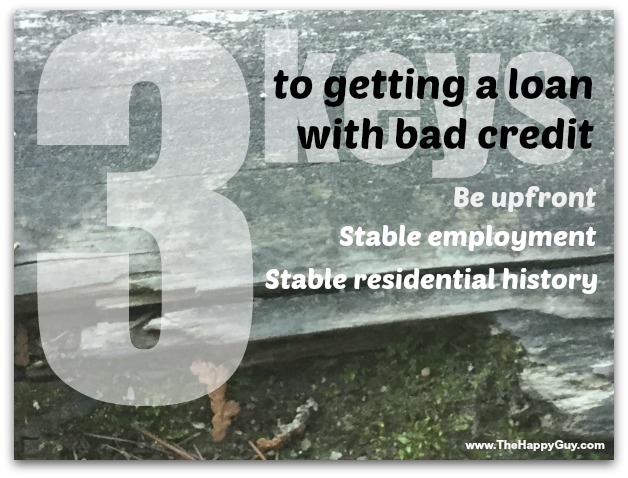

According to this Australian bad credit car loans company, there are three key factors that help you get a loan, even with bad credit:

Be upfront. Bad credit could be the result of dishonesty. Shooting straight makes you a more desirable customer and also saves the headaches of redoing work because you might have been too embarrassed to come clean. Bring as much documentation to show that you are actually a “good credit risk”. If your bad credit was from events of three months ago, show how good a credit you have been since then. Don’t just tell – show. Bring documentation.

Stable employment. This is huge! You might have bad credit, but that doesn’t mean you can’t pay. Being able to show steady income is critical to being seen as a bona fide customer. As this Canadian mortgage company states, “One of the most important factors that lenders look into is proof of sufficient income.” No income, no loan. Don’t try to buy a home. Don’t try to buy a car. Find a homeless shelter until you can get some income.

Stable residential history. Unconventional lenders take on customers they feel will be able to pay back the loan. Steady income is one thing, but being able to find you is another. Get out of the homeless shelter, rent a place, show that you are stable,…then go for the loan.

It goes without saying that anything you can do now to improve your credit rating should be done. Start right away, whether you need that car tomorrow, in six months or in two years. The sooner you start repairing your credit, the sooner you’ll have less to fret over. In fact, Edmunds.com suggests that you “Run it at least three months before you plan on buying so you can take action on any outstanding items.” That’s good advice, because if you can fix or improve even one item, it will make the loan easier to get and could save you hundreds of dollars in interest.

This finance blogger suggests getting a secured credit card right away. Interestingly, this finance blogger suggests sticking to a steady job and staying in one place. It seems that these are not only key to getting a car loan or mortgage, but even to repairing one’s bad credit.

Get pre-approved. The worse your credit, the more uncertain it is how much you will be approved for and what the interest rate will be. Before shopping for a car or a home, find out how much you can borrow and what it will cost you.

Along with getting pre-approved, don’t fall in love with a vehicle or a home ahead of time. Until you know what you can afford, keep your mind – and heart – open.

Source: https://qvcredit.sg/always-choose-reliable-licensed-money-lender-in-singapore/

My credit history got trashed last year after I kept missing my credit card payments as we were buying lots of equipment for our biz. It was great up until that point. Grr.

Found this very helpful, thanks.

Having bad credit doesn’t always discount you from getting a loan. It depends on quite a few things. Sometimes it just depends on the lender – and if they consider you to be too big of a risk. It sometimes depends on the type of event on how long ago it occurred. Sometimes they will give you the loan, but it will be at a higher interest rate. I agree with you that having a stable employment history and residential history is of benefit and being upfront with your issues can be of benefit to you. I do recommend keeping track of your credit report to ensure there are no discrepancies and be in the know of what your score is and be actively working to improve it. Great information, thanks for sharing!